How Real Estate Agent Commissions Really Work

You built equity in your home over years. Maybe decades. And the moment you decide to sell, the default expectation is that you’ll hand 5-6% of your sale price to people you just met.

On a $400,000 home, that’s $24,000. Gone before you ever see a dime of your proceeds.

Most sellers don’t think twice about it. They sign the listing agreement, the house sells, and they see the commission deducted on the settlement statement. It just feels like a cost of doing business. But when you actually trace where that $24,000 goes and who benefits from the structure, the picture gets ugly fast.

And here’s what makes it worse: as of August 2024, the rules changed. The commission system was fundamentally restructured by a landmark court settlement — but most sellers still don’t know it. Agents haven’t been advertising it. The default behavior hasn’t changed. Sellers are still handing over the same fees, just with different paperwork underneath.

The commission split: a four-way chop

When you hire a listing agent, you’re not just paying one person. You’re signing a contract with that agent’s brokerage agreeing to pay 5-6% of the final sale price. That commission then gets divided up. Twice.

Here’s how it works on that $400,000 sale at 6%:

First split: The $24,000 gets divided between the seller’s agent’s brokerage and the buyer’s agent’s brokerage. Assuming a 50/50 split, each brokerage gets $12,000.

Second split: Each brokerage then splits their portion with the individual agent. Again, often 50/50 for newer agents (experienced agents negotiate better splits, but stay with me).

So your listing agent, the person you actually interact with, walks away with about $6,000. The buyer’s agent gets roughly $6,000. And the two brokerages pocket the other $12,000.

You paid $24,000. Four different parties got a cut. Your agent got 25 cents of every dollar you spent on commission.

Why the percentage model is absurd

Think about what 6% actually means at different price points.

Sell a $200,000 house? Commission is $12,000. Sell a $600,000 house? Commission is $36,000. The work involved in selling a $600,000 house versus a $200,000 one is not three times harder. It’s roughly the same listing process, same photos, same open houses, same paperwork.

But you’re paying triple.

A flat-fee attorney will handle your closing for $500 to $3,000. That’s the legal work: contracts, title review, closing coordination. The same legal work your agent’s brokerage charges you thousands for, except they aren’t even the ones doing it. They hire a closing attorney anyway.

So what exactly is the other $22,000 paying for?

The incentive problem nobody talks about

Here’s where the commission model really breaks down. Your agent’s financial incentive is not aligned with yours. Not even close.

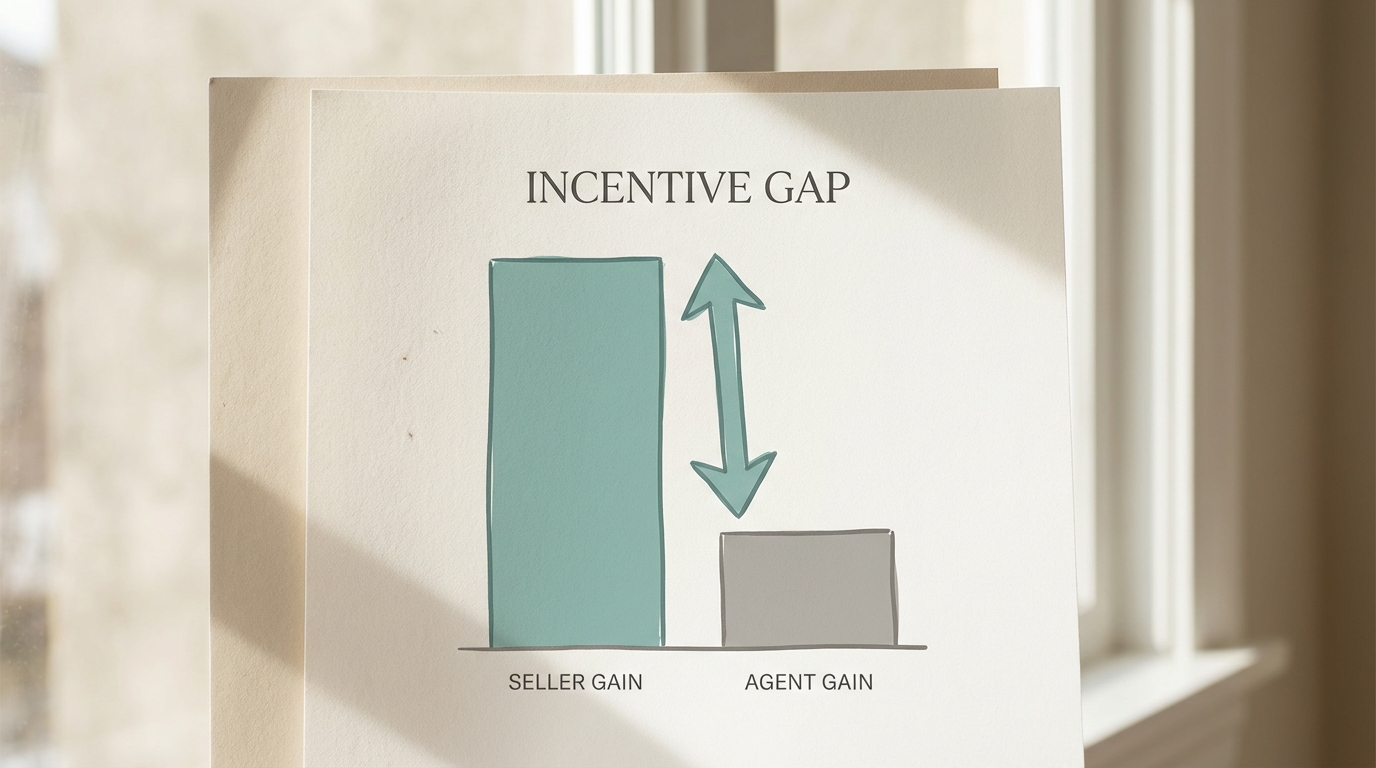

Let’s say you list your home at $400,000. A buyer comes in with an offer at $390,000. You want to hold firm. You believe $400,000 is fair. Your agent suggests you take the $390,000 offer because “a bird in the hand” and “the market could shift.”

Run the numbers on what holding out for $400,000 means for each of you.

For you: The difference between a $390,000 sale and a $400,000 sale is $10,000 gross. After commission, you net roughly $9,400 more by getting your asking price.

For your agent: That same $10,000 difference in sale price, after the double commission split, puts about $150 extra in their pocket.

Your agent is weighing $150 against the risk of the deal falling through, spending more weekends doing showings, and delaying their commission check by weeks or months. You’re weighing $9,400.

No rational person risks weeks of additional work for $150. So your agent pushes you to take the lower offer. They get paid today, and you leave $9,400 on the table.

This isn’t speculation. A 2005 paper from the National Bureau of Economic Research studied this exact dynamic and concluded: “The agent has strong incentives to sell a house quickly, even at a substantially lower price.”

The researchers compared how agents sold their own homes versus their clients’ homes. Agents kept their own listings on the market significantly longer and sold them for more money. When it was their equity on the line, they suddenly found the patience to wait for a better offer.

Do agents actually get you a higher price?

The standard justification for paying $24,000 in commission is that agents get you a better price. Their market knowledge, negotiation skills, and network of buyers supposedly earn back the commission and then some.

Researchers at Stanford tested this claim directly. Their finding: “We find no evidence that the use of a broker significantly affects either the selling price.”

Read that again. No evidence of a significant effect on selling price. Not “a small effect.” Not “a modest effect.” No evidence.

You’re paying tens of thousands of dollars for a service that, according to peer-reviewed research, doesn’t measurably increase your sale price. The entire value proposition of the traditional commission model collapses under academic scrutiny.

The 2024 NAR settlement changed everything

In March 2024, the National Association of Realtors agreed to a $418 million settlement that fundamentally rewrote how real estate commissions work in the United States. The rules took effect in August 2024. Most sellers have no idea it happened.

How it worked before (pre-August 2024)

Under the old MLS rules — in place for decades — sellers who listed on the MLS were required to offer compensation to buyer’s agents as a condition of the listing. When you signed a listing agreement, one of the fields you filled in was the percentage you’d pay to whatever agent brought you a buyer. Typically 2.5% to 3%.

This created what critics called “cooperative compensation”: the seller automatically paid both their own agent and the buyer’s agent. The buyer never saw or negotiated this fee. It was baked into the transaction structure from day one.

The result was a system where buyer’s agents had a financial incentive to steer clients toward higher-commission listings and away from lower ones. FSBO sellers who tried to offer less faced an uphill battle because agents could — and sometimes did — simply not show their homes.

The four-way commission split described above was the direct product of this structure.

How it works now (post-August 2024)

The settlement eliminated the requirement to offer buyer’s agent compensation on the MLS. That field no longer exists. Here’s what changed:

Sellers no longer automatically pay the buyer’s agent. There is no MLS-mandated commission for the buyer’s side. You can offer buyer’s agent compensation if you choose to, but the system no longer requires it as a condition of listing.

Buyers must sign written agreements with their agents before touring homes. Buyer’s agents now need a signed buyer representation agreement before they can show property. That agreement spells out exactly what the agent earns and who is responsible for paying it. The buyer’s agent fee is now a matter between the buyer and their agent — not something that defaults to the seller.

No offers of compensation can be made on the MLS. Under the settlement rules, sellers and listing agents cannot advertise buyer-agent compensation offers on the MLS itself. Any discussion of buyer-side compensation happens outside the MLS — in direct negotiations, in written offers, or as part of the purchase agreement.

Commission is now explicitly negotiable on both sides. The “standard” 5-6% was always a norm enforced by industry pressure rather than law. The settlement stripped away the structural mechanisms that enforced that norm. Sellers can offer 0%, 0.5%, 1%, or whatever they want. Buyers can negotiate their own agent’s fee independently.

What this means for FSBO sellers

If you’re selling FSBO, the settlement is unambiguously good news — and here’s why it matters more for you than for sellers who hire listing agents.

You were already skipping the listing agent’s 2.5-3%. Now you have real leverage on the buyer’s agent side too. The MLS no longer contains any cooperative commission offer that buyer’s agents can see or count on before scheduling a showing. Buyer’s agents who want to bring their clients to your home must have a buyer representation agreement in place — an agreement that addresses their compensation directly with their buyer.

That means when a buyer’s agent calls you asking about commission, they are not negotiating from a position of entitlement. They are asking whether you want to sweeten the deal for their buyer. You can say no. You can counteroffer. You can wait and see what the offer looks like first.

The structural advantage the traditional commission model had over FSBO sellers — the MLS compensation field — is gone. You’re now negotiating on equal terms.

What does this mean in practice? The four-way commission split I described above still exists for sellers who choose to pay it. But “choose” is the operative word now. You have options that didn’t functionally exist before August 2024.

The FSBO savings calculator breaks down the math at every buyer-agent commission level so you can see exactly what you keep under each scenario.

How FSBO sellers can negotiate buyer-agent commission

Post-settlement, here’s the new reality. Every buyer who comes to see your home with an agent has already signed a buyer representation agreement. That agreement spells out what the agent expects to earn — but it does not make you responsible for that fee. The buyer and their agent made that agreement between themselves. You are not a party to it.

Some buyer’s agents will try to make you feel otherwise. They may call before a showing and ask about your “commission offer.” Under the new rules, they cannot see any such offer on the MLS — because none can be listed there. They’re asking because they want to establish one before their buyer gets attached to your house. You don’t have to answer.

The scenarios you’ll encounter:

Buyer asks you to pay 2.5-3% buyer’s agent commission. This is the old way, repackaged. Some agents still push for it. You can say no, counteroffer, or build it into the overall deal evaluation. Run the numbers: on a $400,000 sale, the difference between offering 3% ($12,000) and 1% ($4,000) is $8,000. That’s real money.

Buyer asks you to pay 1-2%. Increasingly common post-settlement. Many buyers negotiate a reduced commission with their agent upfront. If the overall offer is strong, paying 1-2% still saves you thousands compared to the traditional model.

Buyer asks for 0.5% or a flat fee. Some agents will accept a small concession rather than lose the deal. On a $400,000 house, 0.5% is $2,000 — reasonable if the offer is solid.

Buyer handles their own agent’s fee. The cleanest scenario. The buyer pays their agent directly per their representation agreement, and you pay nothing. This is becoming more common with buyers who negotiated flat-fee or hourly arrangements.

The negotiation script that works: When a buyer’s agent asks about commission before a showing, say: “I evaluate compensation as part of the full offer. If your buyer loves the house, let’s talk numbers once we see the complete terms.” This keeps your options open, signals professionalism, and shifts the conversation to where it belongs — the offer itself.

If an agent pushes back with “my buyer’s agreement says I earn 2.5%,” the correct response is: “I understand you and your client have an agreement. That’s between you and your client. I’m happy to discuss whether the seller can contribute to that as part of a written offer.”

The key insight hasn’t changed: every dollar of buyer’s agent commission you pay comes from your equity, just like the listing agent’s commission would have. The savings calculator lets you model different scenarios so you know exactly what you keep at every commission level.

”But buyers won’t see my home without an agent”

This is the fear that keeps sellers locked into the commission model. And there’s a kernel of truth in it. About 86% of buyers purchase through a buyer’s agent, according to NAR’s own data.

But here’s what that statistic doesn’t tell you: those buyers are searching Zillow, Realtor.com, and Redfin on their own. They find the homes. Their agent writes the offer. The buyer’s agent isn’t bringing mystery buyers out of thin air. They’re processing paperwork for buyers who already found your listing online.

Since August 2024, buyers must sign a written agreement with their agent before touring homes — not after finding a home they like, but before the first showing. That agreement addresses the agent’s compensation directly with their buyer. This works in your favor as a FSBO seller. The buyer’s agent is now contractually obligated to show your home if their client wants to see it, regardless of what commission you’re offering — because their compensation arrangement is already settled with their buyer. The old tactic of agents steering buyers away from low-commission listings is much harder to pull off when the buyer has already found your listing on Zillow, signed an agreement with their agent, and told them they want to see it.

You can list on the MLS through a flat-fee service for a few hundred dollars. Your home shows up on every major search site. Buyers find it the same way they’d find it with a full-service listing, by scrolling on their phone.

The brokerage model is built on your money

Brokerages are businesses. They have offices, marketing budgets, franchise fees, and management salaries. All funded by seller commissions.

Keller Williams, RE/MAX, Coldwell Banker. These are massive companies. Their revenue comes from one place: the percentage of your home’s sale price that flows through their agents. Every brokerage split, every desk fee, every franchise royalty traces back to your equity.

Your agent keeps a fraction of what you pay. The brokerage keeps the rest. And the brokerage’s primary interest isn’t getting you top dollar. It’s volume. More transactions, faster closings, steady cash flow. That institutional priority trickles down to every agent who works under their roof.

When your agent pushes you to accept a lower offer, they might genuinely believe they’re giving good advice. But they’re also operating inside a system that rewards speed over price, volume over value, and closing over patience.

What $24,000 could actually buy you

Instead of paying a 6% commission on a $400,000 sale, consider what that money gets you if you sell FSBO:

- Flat-fee MLS listing: $300-500. Your home appears on Zillow, Realtor.com, and every major site.

- Real estate attorney: $500-$3,000. They handle contracts, disclosures, title work, and closing.

- Professional photography: $200-400. The same photographer your agent would hire anyway.

- Home inspection (pre-listing): $300-500. Gets ahead of buyer objections.

Total: roughly $1,300 to $4,400.

That’s a savings of at least $19,000 compared to a 6% commission. Nineteen to twenty-two thousand dollars that stays in your pocket. That’s a year of mortgage payments on many homes. A college fund contribution. A renovation on your next place.

The commission model survives because most sellers never do this math. They assume the 5-6% is fixed, inevitable, a law of nature. It isn’t. It’s a business arrangement, and you can choose a different one.

The real question

Every dollar of commission comes directly from your equity. Not from some abstract pool of money. From the value you built over years of mortgage payments, maintenance, and improvements.

The commission structure was designed by brokerages, for brokerages. The double split ensures the institutions get paid regardless of how hard any individual agent works. The percentage model guarantees that higher-value homes generate bigger paydays for the same amount of effort. And the incentive misalignment means your agent is financially motivated to close fast and move on to the next deal.

So before you sign a listing agreement, pull up a calculator. Type in your expected sale price. Multiply by 0.06. Look at that number. Then ask yourself whether the service you’re buying is worth that specific amount of your money.

If you want to understand what actually goes into selling a home yourself (the paperwork, the pricing, the process), that’s what the rest of this site is for. Run the numbers through the FSBO savings calculator to see exactly what you keep at different commission levels. Then start with how to price your home without an agent, because getting the price right is the single most important thing you’ll do in a FSBO sale.

Keep reading

Florida FSBO disclosure requirements: what you must tell the buyer

Florida FSBO sellers must disclose known material defects plus flood, HOA, property-tax, sewer, radon, and lead-paint notices.

Seller closing costs calculator: estimate your net proceeds

Estimate your seller closing costs, mortgage payoff, and net proceeds with editable state transfer-tax presets and FSBO-specific line items.

The FSBO Savings Calculator: How Much Will You Actually Keep?

At 6% commission, a $400,000 sale costs you $24,000. Here's the real math on what you save selling FSBO, including the costs you'll still have.